The accrual basis can be compared and contrasted to a cash basis, the cash basis being a simplified method, one which does not provide information as useful, as relevant, or as accurate as an accrual method.

What We Need to Know About Cash Basis

Cash basis Records revenue when cash is received and expenses when cash is paid. A cash basis is not the basis required by GAAP, GAAP rules following an accrual basis, but understanding a cash basis helps in understanding both how an accrual basis works and the reasons for it.

When to Recognize Revenue Under a Cash Basis and Why

Cash and revenue are not the same things, as we will see when we record transactions, but a cash basis uses cash as an indicator of when revenue will be recorded. The concept of a cash basis is like a firefighter following the smoke to get to a fire, the smoke not pinpointing the exact location but being close enough. Cash collection does not always equal the exact location in time of revenue earnings but is often close enough.

When to Recognize Expenses Under a Cash Basis and Why

In a similar way as revenue being recorded when cash is received under a cash basis, expenses are recorded when cash is paid under a cash basis. Cash and expenses are also not the same things, as we will see when we record transactions, but a cash basis uses cash as an indicator of when expenses will be recorded. The concept of a cash basis is like a firefighter following the smoke to get to a fire, the smoke not pinpointing the exact location but being close enough. Cash payment does not always equal the exact location in time expenses were incurred but is often close enough.

Very few businesses use a pure cash basis because there are times when the smoke is not close to the fire, times when revenue is not close to cash collection, and times when expense incursion is not close to cash payment. For example, almost any business would recognize a cash payment of $100,000 for a building as an asset of a building rather than an expense of building expense even though cash is paid. The reason a building is recorded as an asset is that the asset has not yet been consumed, has not yet been used to generate revenue.

What We Need to Know About the Accrual Basis

Accrual basis – is driven by two main principles, the revenue recognition principle and the matching principle. Revenue recognition deals with the time to recognize revenue and the matching principle deals with the time to record expenses.

When to Recognize Revenue Under an Accrual Basis and Why

The revenue recognition principle records revenue when the revenue is earned, a time which is not always the same as when revenue is paid. Finding the exact time that revenue has been earned is not always easy but is usually when the job has been completed. For example, the time when revenue has been earned for a service company is when the job has been completed, when the service is done, and the time when revenue has been earned for a merchandising company is when inventory is delivered to the customer. An accrual method is closer to a firefighter using a GPS system to pinpoint the exact location of a fire rather than just estimating the location by following the smoke.

Examples of Revenue Recognition

For example, a food truck may have a policy of only accepting cash for food. The policy of accepting cash as the only form of payment means the time cash is received and the time work is done will be the same. Therefore, both a cash method and an accrual method will result in the same journal entry but for different reasons, the cash method being driven by the cash received, the accrual method being driven by the earnings of the income, by the delivery of the food.

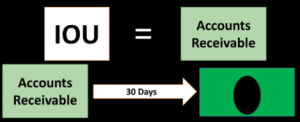

A bookkeeping business, on the other hand, will often need to perform work, invoice the client on completion of the work, expecting a check in the mail sometime in the future. The revenue recognition principle would require revenue to be recognized at the time the work was done, often when the invoice was generated and not when cash was received. We will cover the format of these transactions a little later but for now, recognize that revenue is the act of earning revenue which is different from receiving cash, cash usually being the form of payment for revenue earned. There are other forms of payment, including trade or barter, but cash is the most common form of payment. The revenue recognition principle is similar to how most of us think of our paychecks when working for a company. A business may pay employees every other week, but an employee has earned the revenue in the week the work was done. The company is expected to pay the employee for work done even if the employee leaves the company. For example, if an employee earned wages of $1,000 last week according to their employment agreement and employment is terminated this week the  employee will still expect payment of $1,000 for the work performed last week, for revenue that was earned by the employee last week even though cash had not yet been received.

employee will still expect payment of $1,000 for the work performed last week, for revenue that was earned by the employee last week even though cash had not yet been received.

It is possible, but less common, to receive cash before work is performed, revenue still being recorded at the time work is done under an accrual basis rather than the time payment is received. For example, a newspaper company will collect money before doing the work, before delivering newspapers. A newspaper company will often collect money for a year’s subscription and then earn the revenue by delivering the newspapers in the future. Under an accrual method the newspaper company will have to wait on recording revenue until they earn the revenue by doing work, by delivering the papers, even though they already have the cash in hand. Even though the company has the cash related to future sales they have not earned the revenue for those future sales and if they do not deliver the newspapers in the future they will owe the money back.

Accounting Equation, Account Types, and the Double Entry Accounting System

Obstacles to Learning Accounting are the Same as Those for Learning Music

http://www.youtube.com/c/AccountingInstructionHelpHowToBobSteele

http://accountinginstruction.com/

https://www.linkedin.com/company-beta/18090288

https://www.facebook.com/pg/AccountingInstructionhelp/videos/?ref=page_internal

1 comment