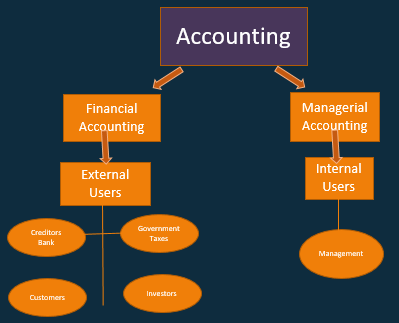

Accounting is divided into two major groups; Financial Accounting & Managerial Accounting.

Financial Accounting – What Needs To Be Known

Financial accounting has the end goal of generating financial statements,  financial statements designed with external user needs in mind. The aim of financial accounting toward external users may seem strange at first because financial data is required and used for internal, managerial, decision making as well but external users have needs that require more reliance on financial statements in many ways.

financial statements designed with external user needs in mind. The aim of financial accounting toward external users may seem strange at first because financial data is required and used for internal, managerial, decision making as well but external users have needs that require more reliance on financial statements in many ways.

External users are users outside the company and include investors, creditors, the internal revenues service, and customers. Companies need these external users for things such as investments, loans, and to follow laws and regulations.

External users do not have intimate knowledge of the business and therefore need assurance to increase the level of trust, trust being a necessary component for business transactions to take place. To increase confidence levels, financial statements are required to follow a strict format of rules designed to standardize the financial reporting. Standardization allows for the comparison of financial information across time and between different companies.

Managerial Accounting-What Needs To Be Known

Managerial accounting has the goal of generating relevant information for  internal decision makers to make sound decisions, for management. Managerial accounting does include the use of the same financial information generated in financial accounting, but information is not required to be in a particular format, managerial accounting being less regulated. Management has intimate knowledge of the company, and therefore there is less need for regulations on the format of data and information. Management will determine the best format for managerial statements to assist in making the best decisions.

internal decision makers to make sound decisions, for management. Managerial accounting does include the use of the same financial information generated in financial accounting, but information is not required to be in a particular format, managerial accounting being less regulated. Management has intimate knowledge of the company, and therefore there is less need for regulations on the format of data and information. Management will determine the best format for managerial statements to assist in making the best decisions.

Because managerial accounting is less regulated, it is commonly thought that managerial accounting will differ greatly from organization to organization. While it is true that managerial accounting practices will vary from company to company, there are also best practices which are applied, practices that have stood the test of time, those that have helped good companies be great. The study of managerial accounting is the study of best practices used to make good business decisions.

Financial accounting developed in much the same way, businesses looking for best practices to compile data for both themselves and external users. Over time financial accounting has solidified those best practices into a standardized form. Standardization often limits innovation but does provide a clear format for external users, this being one of the trade-offs related to regulation. We will talk more about the need for standardization in a profession like account when we discuss what a profession is and the need for ethics and regulations within a profession.

http://www.youtube.com/c/AccountingInstructionHelpHowToBobSteele

http://accountinginstruction.com/

https://www.facebook.com/pg/AccountingInstructionhelp/videos/?ref=page_internal

2 comments