Financial Accounting 3 – Accounting Concepts Continued More Info: Financial Accounting # 1 Link – Accounting equation, debits & credits, adjusting entries, closing process, & inventory transactions. https://youtu.be/slbij2ovIf8 Financial Accounting #2 – Inventory Flow (FIFO, LIFO. . . ), Subsidiary Ledgers (AR AP), Cash & Bank Reconciliations, Allowance method (AR), Depreciation https://youtu.be/B8R7i_GhX-0 Links to points… Continue reading Financial Accounting 3 – Accounting Concepts Continued

Tag: Financial Accounting

Financial Accounting #2 – Intermediate Accounting Concepts

Financial Accounting #2 – Intermediate Accounting Concepts Financial Accounting # 1 Link – Accounting equation, debits & credits, adjusting entries, closing process, & inventory transactions. https://youtu.be/slbij2ovIf8 Links to relevant parts of the presentation. Inventory Costs – FIFO LIFO Weighted Average 1:14 Inventory Tracking 6:52 Inventory Methods Explained and compared FIFO LIFO Ave 15:23 Inventory Costs… Continue reading Financial Accounting #2 – Intermediate Accounting Concepts

Financial Accounting

Financial Accounting – Accounting cycle – We cover most introductory financial accounting topics in detail. Links to relevant parts of the video below. Financial Accounting Overview: 0:17 Why Learn Accounting 19:58 Accounting Objectives 29:22 Accounting Equation 44:36 Balance Sheet 1:01:58 Income Statement 1:15:22 Statement of Equity 1:26:11 Balance Sheet & Income Statement Relationship 1:49:58 Cash… Continue reading Financial Accounting

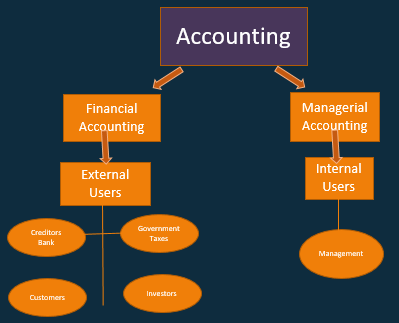

Categories of Accounting – Financial Accounting & Managerial Accounting

Accounting is divided into two major groups; Financial Accounting & Managerial Accounting. Financial Accounting – What Needs To Be Known Financial accounting has the end goal of generating financial statements, financial statements designed with external user needs in mind. The aim of financial accounting toward external users may seem strange at first because financial data… Continue reading Categories of Accounting – Financial Accounting & Managerial Accounting