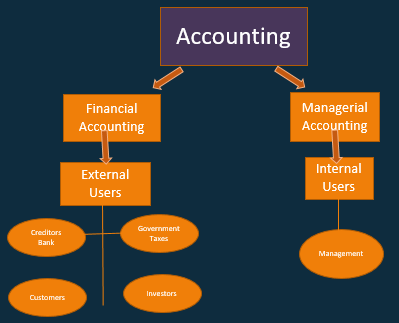

Accounting is divided into two major groups; Financial Accounting & Managerial Accounting. Financial Accounting – What Needs To Be Known Financial accounting has the end goal of generating financial statements, financial statements designed with external user needs in mind. The aim of financial accounting toward external users may seem strange at first because financial data… Continue reading Categories of Accounting – Financial Accounting & Managerial Accounting