Although learning how debits and credits work is not easy the definitions of debits and credits are.

A debit can be defined as “recorded on the left side” (John J. Wild, 2015) and a credit can be defined as “recorded on the right side” (John J. Wild, 2015). Note that these are partial definitions of debits and credits from the text, Fundamentals of Accounting, Wild 22nd, but they are the important parts, the parts that define what debits and credits are, the rest of the definition explaining what debits and credit do.

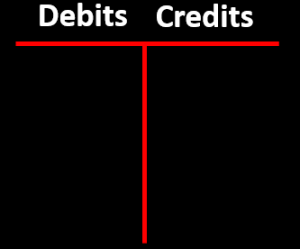

The definition of debits as, recorded on the left, and credits as, recorded on the right, implies something to be recorded on, some kind of board, paper, account, or ledger. A T-account can be imagined as the board, or ledger, used to record debits and credits, the debits being recorded on the left, the credits being recorded on the right.

The definition of debits as, recorded on the left, and credits as, recorded on the right, implies something to be recorded on, some kind of board, paper, account, or ledger. A T-account can be imagined as the board, or ledger, used to record debits and credits, the debits being recorded on the left, the credits being recorded on the right.

Definitions Needed To Record Financial Transactions

When thinking about debits and credits in the context of financial transactions, entering financial data, and creating financial statements the definition above is the only definition we should have in mind. It is difficult to limit our thoughts and definition of debits and credits to the amount recorded on the left or right side of a T account, or ledger, reducing all notions of debits and credits to no more placeholders, similar to the black and red pieces on the checker board. The black and red pieces on a checker board have no real meaning, the pieces in no way holding the rules, or idea, of the game of checkers, but when we see checker pieces we think of much more than black and red placeholders. We think of the game and how it works.

The same is true when we hear the terms, debit and credit, the terms often having a meaning to us which is so much more than the placeholders they actually are. The difference between how the concepts of debits and credits relate to accounting and how the concepts of checker pieces relate to the game of checkers is that most of us learned how to play the game of checkers while also learning the definition of what checker pieces are, but most of us have not fully learned the game of accounting, although we have heard the terms of accounting pieces used in many different contexts, the accounting pieces being debits and credits. The fact that we have learned terms related to debits and credits apart, or outside, of the accounting game leads to false, or incomplete, understandings of what the words mean.

When learning how to record accounting transactions, we need to get back to the core definitions, requiring us first to unlearn definitions we may have picked up in our lives, definitions which may not be complete. These definitions can be revisited and understood from a new perspective once we know how debits and credits are used to record transactions.

How we Learn Incomplete Accounting Definitions and What to Do About it

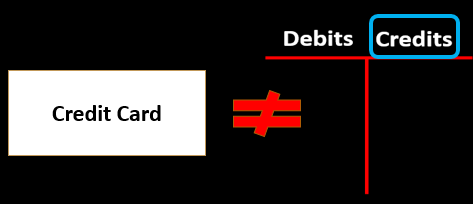

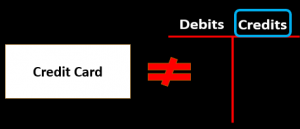

An example of the term credit being used in a misleading, or incomplete, way is  when we think about credit cards, credit terms, or a bank increasing our account with a credit. These uses of the phrase credit are derived from the original meaning of the word, the definition of the amount on the right side, but have come to mean different things to different people. After we learn accounting transactions and see how debits and credits are used in them, we should revisit these terms to understand the origin and evolution of their meaning in different contexts.

when we think about credit cards, credit terms, or a bank increasing our account with a credit. These uses of the phrase credit are derived from the original meaning of the word, the definition of the amount on the right side, but have come to mean different things to different people. After we learn accounting transactions and see how debits and credits are used in them, we should revisit these terms to understand the origin and evolution of their meaning in different contexts.

An example of how life experiences can lead to an incomplete understanding  the terms debit and credit is a bank agreeing to eliminate a charge on a customer’s balance by saying they will credit the customer’s account. This transaction causes the customer to think of the term credit as a good thing, an increase in their checking account balance. While the credit does represent an increase to the client balance the accounting definition of credit is an amount reported on the right side of a T account or ledger, the bank reporting an amount on the right side of their ledger. When we see the bank statement, we see the bank recording credits as an increase to our account balance but from the bank perspective increases to our account balance are not assets but liabilities, representing the bank owing money to the customers.

the terms debit and credit is a bank agreeing to eliminate a charge on a customer’s balance by saying they will credit the customer’s account. This transaction causes the customer to think of the term credit as a good thing, an increase in their checking account balance. While the credit does represent an increase to the client balance the accounting definition of credit is an amount reported on the right side of a T account or ledger, the bank reporting an amount on the right side of their ledger. When we see the bank statement, we see the bank recording credits as an increase to our account balance but from the bank perspective increases to our account balance are not assets but liabilities, representing the bank owing money to the customers.

To Learn Accounting Transactions Trust the Definition of Debits and Credits

As we learn how to record debits and credits, the definition of debits as just an amount recorded on the left side of the T account or ledger and credits as just the amount recorded on the right side of the T account or ledger, is another area we ask learners to have faith in the system, to trust that these simple definitions are correct. Having patience and holding back on analyzing other preconceived definitions of debits and credits until after we have learned how to record transactions often helps prevent these preconceived definitions from slowing down the learning process. Once we understand the accounting game and how debits and credits are used to play it, we will be better equipped to fully understand any definitions we previously had about debits and credits and analyze how they line up, or fit within, the definition of debits and credits and how debits and credits are used.